As the first quarter of 2026 approaches its end, security dealers find themselves in a market defined by resilience and rapid change driven by technology innovation, new competitive pressures and evolving customer expectations.

The core fundamentals of the industry remain strong, even as dealers note constrained consumer spending and inflation as critical challenges. Installation activity has rebounded after pandemic-era disruptions, system ownership among U.S. households has recovered and demand for connected security systems continues to expand.

New research from Parks Associates, conducted in partnership with Security Sales & Integration, captures the perspectives of more than 200 security dealers across the United States and Canada. The survey, now in its 12th year, reveals an industry that is adapting quickly to competitive pressure from DIY brands while also expanding into new services, technologies and commercial opportunities.

Dealers today face a balancing act: maintaining their traditional strengths in professional installation and monitoring while evolving toward video-driven systems, AI-enabled services and hybrid installation models.

Across the industry, several strategic themes are emerging:

- Diversification of revenue through commercial projects and service add-ons

- Increased focus on video, smart home devices and AI capabilities

- Operational modernization through digital sales channels and automation

- Continued consolidation as investors pursue scale in a fragmented market

The result is a dealer channel that remains vital to the security ecosystem—but one that must continually adapt to stay competitive.

Security Dealers Balance Stability with Growth Expectations

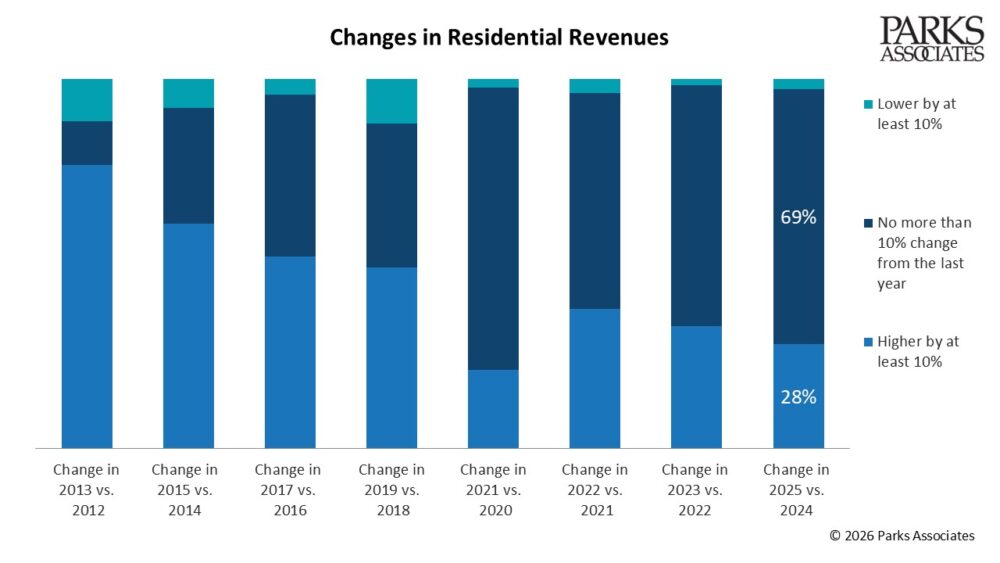

Compared to the dramatic shifts experienced during the pandemic years, dealer outlook for 2025 and 2026 reflects a more stable and cautious growth environment.

In earlier years of the survey, many dealers expected annual growth exceeding 10%. Today, expectations have moderated, with most dealers anticipating revenue changes within plus or minus 10 percent. This shift reflects a more mature industry where growth is steady but shaped by economic factors such as housing market activity, tariffs and inflation-related costs.

Image courtesy of Parks Associates

Despite these constraints, installation activity has recovered. Dealer-reported installations declined between 2019 and 2022 but rebounded beginning in 2023 and approached pre-pandemic levels again in 2025. At the same time, consumer-reported adoption of home security systems has climbed back to roughly one-third of U.S. households.

Dealers are also getting bigger. Over time, the share of companies reporting annual revenues of $3 million or more has increased, while the number of firms reporting under $1 million has declined. Larger and regional players are focused on scaling their operations by expanding geographically or through acquisitions. 54% of owners report that they have been approached with offers to buy their business.

Several forces are contributing to this evolution:

- Increased consolidation within the dealer market, as seen by companies like Pye-Barker and Zeus Security

- Private equity investment seeking recurring revenue businesses, as shown by GTCR’s acquisition of SimpliSafe and ADT multifamily business through Everon

- Expansion into commercial projects with higher contract values

- Greater operational efficiency enabled by technology

While optimism remains tempered compared to earlier years, dealers largely see a stable path forward—provided they continue adapting to new technologies and customer expectations.

Commercial Security Becomes a Major Growth Engine

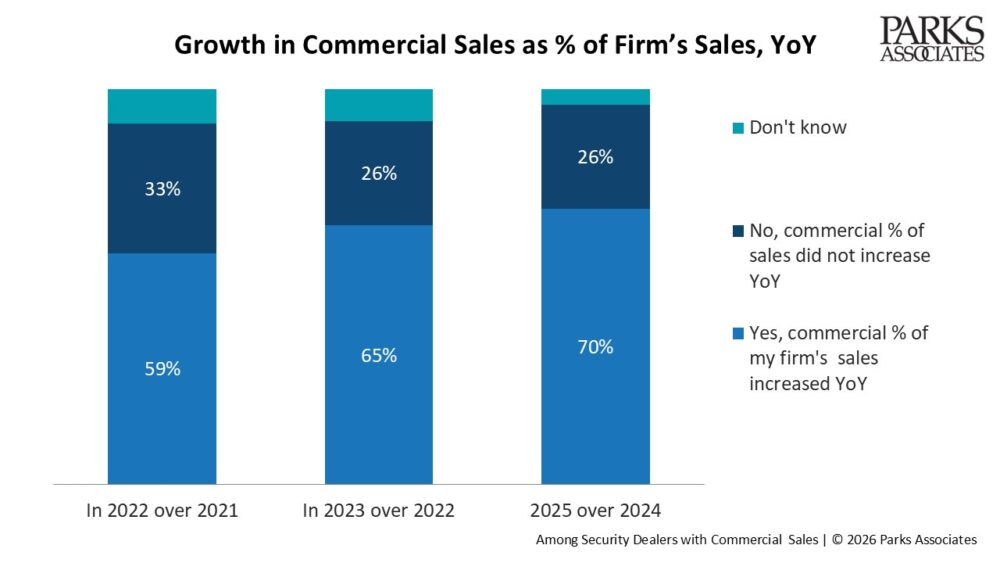

Perhaps the most notable shift in the dealer landscape is the growing importance of commercial security. Historically, residential installations dominated dealer portfolios. Today, that balance has shifted significantly. On average, dealers report that 57% of unit sales are now non-residential, and more than half of dealers say residential accounts account for less than half of their total revenue.

Dealers report that commercial projects often provide larger contracts, longer service relationships and stronger margins. And, among those having at least some commercial business, 70% report that commercial sales are growing as a share of their overall business.

Image courtesy of Parks Associates

Commercial systems are also evolving beyond traditional intrusion detection. Dealers report that the most common commercial offerings include video surveillance systems, access control, fire and life safety systems and video verification services.

Dealers are also closely watching emerging opportunities in the commercial segment. Mobile surveillance units, for example, are gaining attention for temporary security needs such as construction sites and events. Major brands are entering the category as well, highlighted by Ring’s planned mobile security trailer launch in 2026.

Still, most dealers remain cautious about expanding too far beyond their core competencies. Interest in adjacent services such as cybersecurity, EV charger installation, or on-site guard services remains relatively limited compared with traditional security offerings.

Residential Security Evolves Around Video and Smart Home

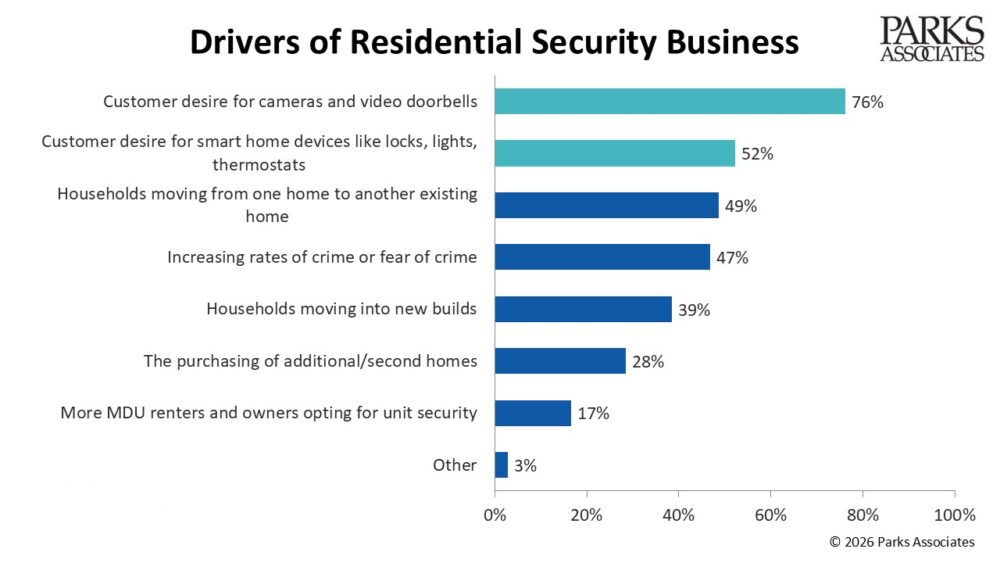

Even as commercial projects expand, residential security remains a foundational part of the dealer business. But the nature of residential systems is changing rapidly. For decades, intrusion detection, including door sensors, window sensors and central panels, served as the core of residential security. Today, video and smart home devices are increasingly the primary driver of system purchases.

Dealers report that consumer demand for cameras and video doorbells is the top trigger for residential security adoption. At the same time, consumer research consistently shows that interest in smart home devices and automation is a leading motivation for purchasing security systems.

Image courtesy of Parks Associates

In practice, this means the modern residential security system is evolving into a broader connected-home platform. Interactive systems now account for more than 80% of residential installations, and recent buyers are more likely to have acquired a camera as part of their system than door/window sensors.

Consumer expectations of what a security system is and should provide have shifted. The camera is the core of the system, and the system value is deepened with home automation devices and AI. Dealers must sell a connected, secure life that makes household management easier. Yet despite selling smart home products, many dealers still position themselves primarily as security providers. Only about 28% identify their businesses as smart home solution companies. Some 72% consider themselves a premise security company.

This disconnect highlights a potential opportunity. As consumers increasingly see security systems as part of a broader smart home ecosystem, dealers who embrace this expanded value proposition may unlock new growth.

DIY Competition Pushes Dealers to Adapt

Perhaps the biggest disruption in the residential market comes from the rise of DIY security systems. Brands such as Ring, SimpliSafe and Arlo have transformed consumer expectations around pricing, installation and purchasing. Online sales, self-installation and flexible monitoring plans have become common features of the DIY model.

Dealers are feeling the impact. Nearly three-quarters (74%) report losing sales to DIY security systems or standalone devices like cameras and video doorbells, a significant increase from previous years. Parks Associates market forecast work projects continued strength in device-first adoption, DIY systems and subscription-based services attached to smart video products, with stronger growth for DIY systems than pro-installed systems through 2030.

Many dealers are not resisting the trend, they are adapting to it. First, more dealers are offering an easier path to purchase by selling product online (36% versus only 24% in 2023). Call-ins from prospects and partnerships with builders, realtors and remodelers remain the most common sales channels, in a misalignment with how consumers purchase nearly all other consumer technology products and home services today – online.

The growth in online selling by dealers is a positive trend that and will be increasingly important for dealers to attract new accounts.

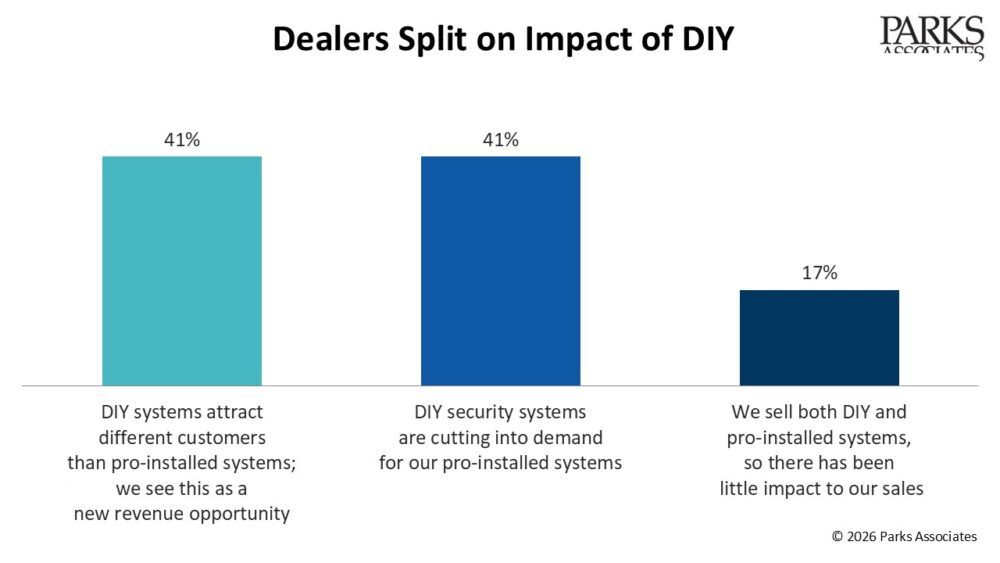

Dealers are also pivoting and offering self-installable systems as 41% of respondents say they are embracing DIY solutions as a way to attract new customers, particularly renters or younger households seeking flexible options.

Image courtesy of Parks Associates

Hybrid approaches appear to be gaining traction as leading brands expand a choice of offerings. ADT expanded from pro into self-setup options while both Ring and SimpliSafe have expanded dealer-focused offerings. Dealers offering self-install systems report that roughly half of their installations are DIY, while the other half remain professionally installed.

This suggests that convenience alone does not replace the value of professional expertise. Instead, the future market will be defined by flexible models that combine DIY convenience with professional service when needed.

Recurring Revenue Expands Through Service Innovation

While hardware remains important, dealers increasingly focus on services to grow recurring monthly revenue (RMR). Security packages have evolved dramatically over the past decade, layering new capabilities on top of traditional monitoring. Today’s premium packages may include video verification, smart home devices and automation, AI-enabled video analytics, cloud video storage and fire and CO monitoring.

These features significantly increase revenue potential. On average, the difference between basic monitoring and a fully featured smart home security package can reach more than $30 per month in additional fees.

Video verification services are becoming particularly important. By allowing monitoring centers to confirm alarms using camera footage before dispatching emergency responders, these systems reduce false alarms and improve response efficiency.

This is quickly becoming table stakes and dealers are looking for more innovative models to enrich the value of professional monitoring. Remote video monitoring and remote guard talk-down takes video verification to the next level, with the latter allowing agents to talk to persons of interest to clarify intentions and deter bad acts.

Image courtesy of Parks Associates

More challenging are new models that upend the economics of monitoring – either by allowing as-needed monitoring or requiring staff to respond on-site. The former undermines the certainty of the revenue stream, and the latter requires high-cost labor. Both are likely to become more common as DIY solutions offer no-contract and ad hoc monitoring and premium guard response becomes necessary in municipalities limiting law enforcement response.

Dealers Embrace AI for Operations and Customer Benefits

Dealers are proactively messaging AI benefits to both residential and commercial customers – a dramatic departure from 2023 strategies. In 2023, only 15% of dealers said they highlighted AI benefits in customer messaging; by 2025 that jumps to 39% for residential and 40% for commercial customers.

Parks Associates consumer data confirms security system owners are among the most AI-positive US consumer segment, as many value the AI enhancements that make their systems and cameras work better (e.g., person detection, smart video search).

Image courtesy of Parks Associates

Dealers are also using AI internally for operational efficiencies. Some 51% of dealers use AI tools like ChatGPT to help craft messaging, 37% use AI for insights on how their customers are using their systems and devices and 29% are using AI to flag customers at risk of cancelling.

These more sophisticated applications of AI for subscriber management and customer support can help dealers modernizing their operations and stay competitive.

Consolidation and Tech Will Shape Security Dealer Market

Looking ahead, the security dealer channel is likely to experience continued consolidation alongside ongoing technological transformation.

The industry remains highly fragmented, with many small regional operators. Private equity firms and larger security platforms are actively acquiring dealers to expand geographic coverage and increase recurring revenue bases. At the same time, technology innovation is redefining the competitive landscape. Future differentiation will likely come from:

- AI-powered monitoring and analytics

- Advanced video capabilities

- Integrated smart home platforms

- Hybrid DIY and professional service models

- Expanded commercial security solutions

For dealers, success will depend on balancing innovation with the core strengths that have long defined the channel: local service, trusted relationships and professional expertise.

The security market is evolving rapidly, but the dealer community remains at the center of delivering secure, connected environments for homes and businesses alike.

This is an excerpt from Parks Associates research study: Security Dealers Perspectives: Views from the Front Line.

Jennifer Kent is senior vice president and principal analyst at Parks Associates.

https://www.securitysales.com/insights/security-dealers-navigate-changing-market/617507/